Mobile Wallets – What Can They Do and What Do You Need?

Following up on our previous blog covering the different types of mobile wallets, and which one suits your situation, we are examining their functional requirements and what can be done to enhance their user experience. This is an excerpt from our guide to mobile wallets which you can download from our resources section.A lot of our customers approach us wanting to offer a mobile wallet to their customers without knowing the requirements or a wallet's true potential. That is quite understandable because once you have decided which mobile wallet is right for you, the requirements and features can change.

Let’s have a look at the components you absolutely need in your tool belt and additional bells and whistles that can make the lives of you and your customers a lot easier.

Tokenization (OEM wallets and Issuer wallets – required)

To digitize your cards for use in a wallet, they must go through a process called tokenization. Payment tokenization is a security technology where sensitive card information is replaced with a unique digital identifier (a token) to process payments without the need to expose card data.

Another significant security benefit of tokenization is the fact that a token is only valid in a specific context. Outside that context, the token is useless and cannot be misused. In practice, this means that a card account can have multiple tokens used for different purposes, e.g., one token for your mobile wallet, one for your smartwatch, and one for a streaming service or a travel ticket app.

All major payment schemes like AmEx, Mastercard, and Visa have developed their own tokenization systems to support card tokenization and require that you have the means to turn your cards into tokens in place.

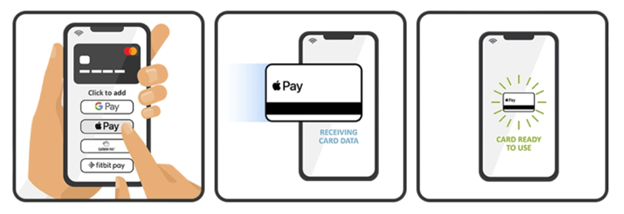

Push provisioning (OEM wallets – required l Issuer wallets – recommended)

There are two ways a cardholder can add their card to a digital wallet.

- The manual way will require all involved parties (wallet provider, scheme, issuer, and cardholder) to follow up with a tedious and time-consuming verification process to ensure the legitimacy and authenticity of adding a card. This process leads to a higher threshold for the cardholder to engage. The reasons could be a lack of trust in the system, worrying about making mistakes, and failure to follow up on the required step-up ID&V process.

- The alternative is called push provisioning and is often required by OEM wallet providers. Push provisioning simplifies and accelerates card issuance to digital wallets for the cardholder and helps wallet providers to acquire new customers. Instead of having to go through a lengthy authentication process and manually entering credentials, users can just push a button on their phone to activate their token.

Typically, this simplified onboarding results in two to three times as many successfully tokenized cards to digital wallets compared with manual onboarding.

Token management solution (Issuer wallets – required I OEM wallets – N/A)

Tokens are created faster and more regularly than ordinary payment cards. After a while, the large number of tokens will be challenging for your customer support to keep track of.

If you build your tokenization platform or buy it from a third party, make sure there is an easy-to-use, efficient, and transparent solution in place that lets customer support easily access token data and manage them.

At the higher end, token management solutions sport built-in analytics and reporting tools that let you gather information on how your customers use tokens and identify opportunities for improvement or new business.

Consumer controls (Issuer-branded wallets – optional)

Today's consumers expect to easily control all aspects of their daily lives in real-time, 24/7, safely, and comfortably from their smart devices.

Consumer controls allow your customers to manage their tokens on their own. The functions can range from activating, suspending, and deleting tokens, to more granular customizations such as defining how much money can be spent where, when, and how.

Thus, consumer controls both enable the cardholder to quickly handle simple token-related tasks without having to call the issuer, while reducing the workload for the issuer’s customer service. In addition, the enhanced user experience and customizability add incentive to increase the usage of the issuer’s mobile or web app for payments and engaging with other services.

Digital Cards (OEM & Issuer-branded wallets – optional)

Digital cards are a digital version of physical payment cards, which can be viewed via a mobile app. Having digital card functionality is not required for mobile wallets, but they can complement a card issuer’s offering, especially if they’re a digital-first bank.

Since not every e-commerce site offers the opportunity to pay with a mobile wallet, a digital card supplies all the information needed to conduct the payment, such as the PAN, expiry date, and CVV code.

If you cannot or do not want to issue a physical card (to save money or better, the environment), or just want to offer your customers a convenient and more secure alternative to their physical card, we recommend considering digital cards.

Now that we’ve had a look at the functional requirements for mobile wallets as well as some value-adding options, we are ready to dive into the implementation. Our next blog will focus on how long it takes to implement a mobile wallet and what parties are involved.

You can also download our guide ' How to get started with mobile wallets'.

FAQ: Mobile Wallets – What Can They Do and What Do You Need?

What is tokenization and why is it important for mobile wallets?

Tokenization replaces sensitive card information with a unique digital identifier (token) to securely process payments. It enhances security by making tokens valid only in specific contexts.

What is push provisioning and why is it recommended?

Push provisioning simplifies and speeds up adding cards to digital wallets, requiring minimal user input, which increases successful tokenization compared to manual methods.

What is a token management solution and why do you need it?

A token management solution helps track and manage the numerous tokens created, ensuring efficient customer support and offering analytics for business improvement.

What are consumer controls and how do they benefit users?

Consumer controls allow users to manage their tokens, such as activating, suspending, and deleting them, which improves user experience and reduces the issuer's customer service workload.

What are digital cards and why might you consider them?

Digital cards are virtual versions of physical cards accessible via mobile apps. They provide a convenient, secure payment method, especially useful for digital-first banks or to replace physical cards.

How do I choose the right mobile wallet for my needs?

When selecting a mobile wallet, consider factors like security features, user experience, compatibility with your existing systems, and support from the wallet provider.

What are the main security concerns with mobile wallets and how are they addressed?

Mobile wallets face security threats such as data breaches and fraud. These are mitigated through encryption, tokenization, biometric authentication, and regular security updates.

How can I ensure a smooth onboarding process for my customers?

Implement push provisioning to simplify adding cards to wallets, provide clear instructions, and ensure robust customer support to handle any issues quickly.